The Cure: How Tackling Waste and Abuse in Annapolis Could Eliminate the State Debt and Release a Billion Dollars a Year for Tax Cuts

About the Authors

Paul O. Ballou III, C.P.A.

Until very recently, Paul O. Ballou III served the 188 members of the General Assembly in a number of capacities, namely, fiscal-note writer, committee staffer, budget analyst, trainer in statistical quantification skills and coordinator for public speaking. His areas of expertise include: taxes, transportation, pension systems and education. Mr. Ballou holds an M.B.A. degree and a B.S. in accounting, both from the University of Kentucky. He is also a certified public accountant. He worked for the General Assembly and the Department of Legislative Services for nine years.

William R. Miles, M.S.

For 17 years, William R. Miles served in the General Assembly as a committee staffer, bureau chief of the fiscal-note system and then principal policy advisor for two speakers of the Maryland House of Delegates, R. Clayton Mitchell, Jr. and Casper R. Taylor, Jr. Mr. Miles’ areas of expertise are: taxes, budgetary and fiscal policies, and the environment He holds a B.A. degree in government and economics from the University of Maryland at College Park and a masters of finance degree from the University of Oklahoma. He now runs his own consulting firm, which specializes in performance measuring for government entities, statistical surveys and strategic planning.

Douglas P. Munro, Ph.D.

Douglas P. Munro has been involved in public-policy issues for a number of years. He completed his doctoral dissertation at the Johns Hopkins University in Baltimore in 1992. He then served as a researcher at the Heritage Foundation in Washington, D.C. and, later, as the senior policy analyst at the Southern Governors’ Association. During this period, he conducted extensive research into the cost of federal mandates on state government for the Wisconsin Policy Research Institute in Milwaukee and the Goldwater Institute in Phoenix, Arizona. In 1995, Munro co-founded the Calvert Institute for Policy Research, Inc., of which he is the president. The institute is Maryland’s first independent, market-oriented research institute, or “think tank,” to focus exclusively on state and local concerns.

|

| From left to right, authors William R. Miles, Douglas P Alunro and Paul 0. Ballou HI. The analysts propose a plan to eliminate the state general obligation debt entirely and free up over $1 billion for tax cuts. |

Executive Summary

A casual approach to the cost and size of government has been a tradition in Maryland. State and local personal income taxation is among the very highest per capita in the country, a fact that has elicited remarkably little interest among the intelligentsia. This is despite a recently published warning by the Glendening administration’s own secretary of business and economic development, James Brady, that such confiscatory fiscal policy serves as a “red flag” to businesses. Secretary Brady has since resigned, and virtually no headway has been made on his recommendation that income taxes be cut by 25 percent by 2005. Governor Glendening’s much-publicized 10 percent tax cut has turned out to be no such thing. After the General Assembly got through with the bill in 1997, the scope of the rate reduction had been whittled down to five percent. The fact is, discussions of fiscal policy in Maryland revolve almost exclusively around questions of revenue. Expenditure reductions are rarely mentioned. The governor’s modest tax-cutting program, for example, has been financed entirely through revenue surpluses. No program cuts have been announced. In an election year, we may rest assured that none will be.

Meanwhile, the state continues to run up debt on stadiums and the like. By the end of this fiscal year (FY 1999), the cumulative debt will stand at $3.5 billion, necessitating $418.5 million in debt-service payments. By 2007, the debt will be $4.5 billion, requiring $633.5 million in maintenance payments. This is not discussed in polite society.

This is Annapolis’ way. Calvert’s proposal stands in stark contrast. It is targeted. It is precise. While modest as a proportion of overall state spending – five percent of this year’s budget – the cuts we identify are nonetheless of greater magnitude than anything proposed by recent legislative or gubernatorial commissions. Unlike other commissions, we identify specific programs and agencies for termination. Due to Calvert’s novel approach, described below, our cuts leverage the largest tax cut in Maryland history – far out of proportion to our program cuts.

Our recommended program cuts and interfund transfers total $870 million in the first year and $634 million a year thereafter. The twist that sets this study apart is that we do not propose sinking our cuts into tax reductions, not directly at least. Rather, the state should use our savings to buy back all outstanding general-obligation debt.

As any credit-card holder knows, paying down your outstanding balance reduces your monthly minimum principal and interest payments. Our plan works in the same way: Pay off the debt and return the money saved on debt-service payments to the public in the form of tax cuts. Over the long run, this leverages tax cuts of greater size than would be achieved by returning the savings directly to taxpayers. In its first year, the Calvert plan could leverage funds for a tax cut of $321.5 million. By 2007, this tax-cut figure would have escalated to $1.03 billion. Annual funds for tax cuts would grow after that. This is because the difference between Annapolis’ planned, ever-mounting debt-service expenses and Calvert’s nonexistent debt-service costs would become larger with every passing year. It is this difference that funds the Calvert tax cuts.

To pay for our plan, we identify a series of program cuts and interfund transfers. Many of our recommendations have been previously identified by various government agencies as areas ripe for targeting. This is probably the most disturbing aspect of our findings: not that the state annually squanders millions of dollars on programs of doubtful worth, but that it does it in the full knowledge that it is doing so. To be wrong in ignorance is one thing; to be wrong and fully aware of it is entirely another. Some highlights of our program cuts:

- School districts’ “over billing” of Annapolis for intergovernmental funding for nonexistent students. This ranges from $10.3 million by Baltimore City to $28.5 million by the already lavishly funded Montgomery County. We recommend a systematic audit of all school-district claims, for a projected annual savings of $179 million (pp. 44-47).

- State agencies’ “over billing” of the government for nonexistent employees. By minimizing expected vacancy rates, agencies receive some $93 million a year more than they are properly entitled to. We recommend that agencies be forced to utilize historical precedent to project vacancy rates (pp. 29-33).

- The “prevailing wage” mandate upon public-sector construction projects. This forces contractors to pay inflated union rates, forcing up costs by as much as 15 percent. We build upon a Department of Legislative Services analysis to project an annual savings of $38.6 million upon the repeal of the prevailing-wage statute (pp. 37-38).

- Maryland funds three preservation programs with similar aims: Program Open Space (POS), the Agricultural Land Preservation Program and Rural Legacy. Maryland should reduce its involvement in the real estate business by terminating state subsidy of county land purchases under POS. County governments are now very fiscally healthy. If preservation is vital to them, they may use their own funds, saving taxpayers $24.2 million (pp.49-51).

- In addition to the regular Maryland State Retirement Agency, which administers state employees’ pensions, the state funds an entirely separate Teachers’ and State Employees’ Supplemental Retirement Agency. This hopelessly duplicative agency should be terminated, for an annual savings of $1.1 million (p. 61).

These plus other savings make up a total of $870.3 million in the first year and $635.8 million after that. This is the price of over $1 billion in tax cuts – an outstanding rate of return.

– Douglas P. Munro, Editor

I. The Maryland Disease

Back in the 1970s, a series of Labour and moderate Conservative governments in the United Kingdom ushered in a period of expanding government, high inflation, massive budget deficits, incessant industrial disputes, low growth and ever-present general economic malaise. It was known at the time as the “British disease.” While hardly in the same league, Maryland exhibits certain similarities. The state government’s penchant for growth is unchecked, while private-sector growth remains relatively flat, at least compared to Maryland’s immediate competitors. From April 1997 through April 1998, employment within the state grew by 1.0 percent. Certainly, any growth is welcome. However, the national rate of employment growth over the same period was 2.0 percent. Two of Maryland’s most immediate competitors, Virginia and Delaware, saw their employment grow by 3.0 percent and 3.5 percent, respectively.1 This has been a chronic problem for Maryland, whose business climate is often held to be hostile, so much so as to merit a lengthy recent report published by the state Department of Business and Economic Development.2 This, then, is the Maryland disease – a disease characterized by high taxes, escalating state debt and unchecked spending mandated under state law.

This paper proposes a cure for the disease. Over the ensuing pages, we shall outline a strategy for entirely eliminating the state general-obligation debt – now $3.3 billion and rising – while simultaneously freeing up enough funds to provide for the largest personal income-tax cut in Maryland history. We achieve this by identifying millions of dollars of wasteful expenditures on programs of doubtful merit. Under our plan, these funds would be redirected to buying back all outstanding state general-obligation debt over the course of two gubernatorial terms, $870.3 million in the first year and $635.8 million a year thereafter. This purchasing of the debt will make funds available for tax cuts by reducing, ultimately to zero, the annual state appropriation necessary for debt-service payments. If our plan is followed through, starting in fiscal year (FY) 2000 funds will be available for some $321.5 million in tax cuts. By FY 2006, this annual tax-reduction figure will have risen to $1.02 billion, increasing to $1.03 billion the following year.

Background

Maryland was rocked by recession from 1991 through 1993. State lawmakers were forced to make cumulative cuts from baseline of $2.1 billion during the three-year period. (“Cuts from baseline” refers to cuts from previously projected expenditure levels, including expected budget increases for inflation, program expansion, etc.)3 Programs were eliminated, entitlements were reduced, some employees lost their jobs and some local-aid programs were terminated.4 This unprecedented action was necessary for Maryland to comply with its constitutional mandate for an annually balanced operating budget.

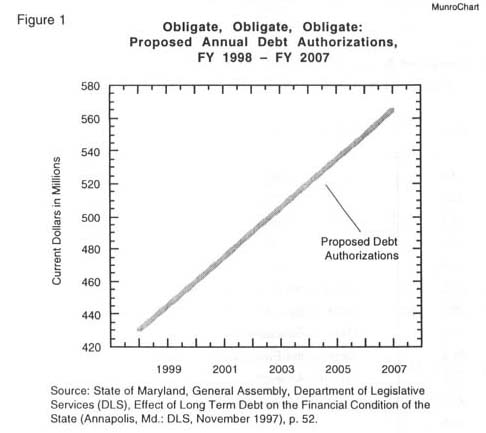

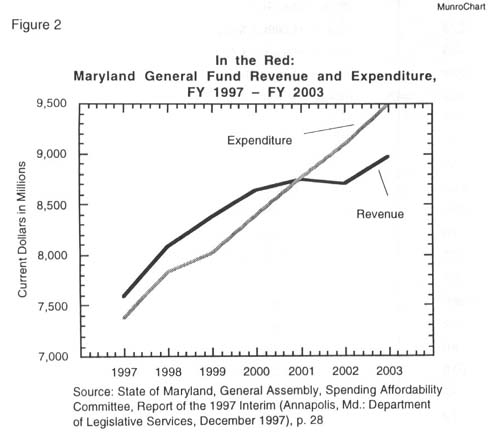

These days, modest annual growth for Maryland is projected for the next few years, as shown in table 1. However, acceptable performance for the moment should not blind policy makers to the serious long-term structural problems facing this state. Maryland’s current cumulative debt as we enter FY 1999 is $3.3 billion, a figure anticipated to rise to $4.5 billion by the end of FY 2007.5 Principal and interest payments on the $3.3 billion debt were $417.8 million in FY 1998.6 These annual payments will rise to $633.5 million in 2007 if the cumulative debt reaches the figure anticipated. Meanwhile, the projected annual debt authorization for 2007 is $565 million,7 a sum 31.3 percent higher than fiscal 1998’s borrowing of $430 million. This ever increasing debt load is being fueled by new borrowing recommended year after year, as shown in figure 1.8 With nearly $1 of every $2 of state expenditure mandated by law, and thus subject to relatively little scrutiny, general-fund expenditures in Maryland will soon outpace revenues, as shown in figure 2. The graph illustrates that by FY 2003, Maryland will be facing a structural operating deficit of $514.5 million (i.e., the gap between the two lines).9

{kind=link}

{kind=link}

{kind=link}

Spending must be, in a word, cut. Maintaining Maryland’s penchant for high spending has two particularly unfortunate side effects (in addition to the straightforward frittering away of public funds on projects of dubious worth). First, it forces the state to keep borrowing funds, thus eternally ratcheting up debt-service costs. Second, it provides a ready excuse to deny tax cuts to state residents. “We urge legislators not to get caught up in a tax-cut frenzy,” the Baltimore Sun recently intoned sternly. “Are they setting Maryland up,” it asked, “for a return to massive shortfalls when the economy fizzles instead of sizzles?”10

This would be a rational warning were it not for faulty underlying logic. The assumption is that annual state expenditure is currently justifiable and, thus, that the only question is how to finance it. By means of indirect revenues generated by a healthy economy? Or by direct means of high state income-tax levels? The establishment fears too much reliance upon the former in preference to the latter. But this fear is based upon a supposition that something akin to current levels of revenue must annually be raised to support current levels of expenditure. We contend that neither is necessary.

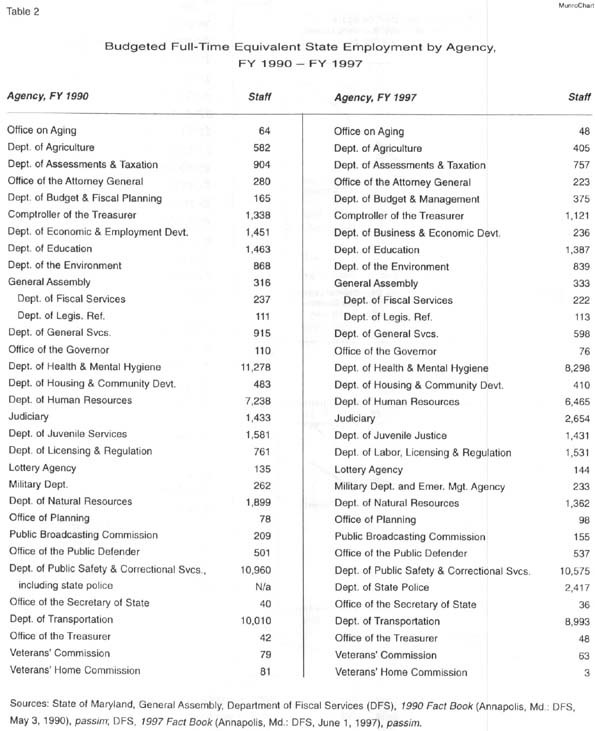

We identify a series of program cuts and propose a debt-elimination strategy that would, in combination, annually save hundreds of millions of dollars without significantly reducing the delivery of necessary services. How does this differ from the cuts made in the early 1990s? Those cuts were cuts within the existing paradigm. Few, if any, serious structural changes were made in Maryland state government. According to the figures shown in table 2, most state agencies now claim fewer employees than they did in FY 1990. These data are misleading, however, for they exclude what are known as “contractual employees,” who technically are not state employees. Such individuals make up an increasing proportion of the state’s work force.

{kind=link}

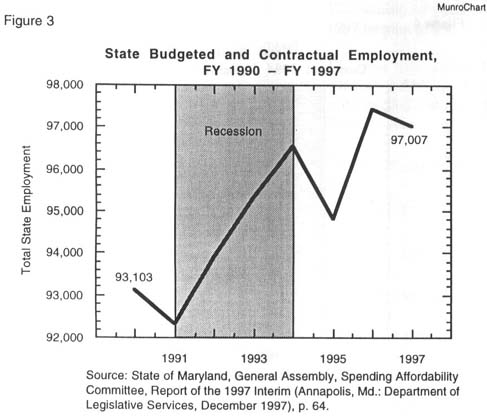

In FY 1990, state contractual workers, University of Maryland contractual workers and General Assembly temporary staff numbered 16,689, which was 22.4 percent of the number of regular state employees. By FY 1997, this had all changed. That year, contractual workers numbered 22,760, the equivalent of 31.8 percent of the regular state work force.11 The advantage of contractual workers is two-fold. First, they are cheaper, as benefits are not included in their compensation packages. Second, the utilization of contractors allows the state to claim it has reduced the number of “state employees” while at the same time actually increasing the state work force. Figure 3 tells the true story. Before the recession, in FY 1990, the state payroll stood at 93,103 (state and contractual employees combined). By FY 1994, immediately after the recession, the payroll for budgeted and contractual employment had reached 96,540 (then going on to hit 97,007 by FY 1997, an increase of 4.2 percent since 1990).12

{kind=link}

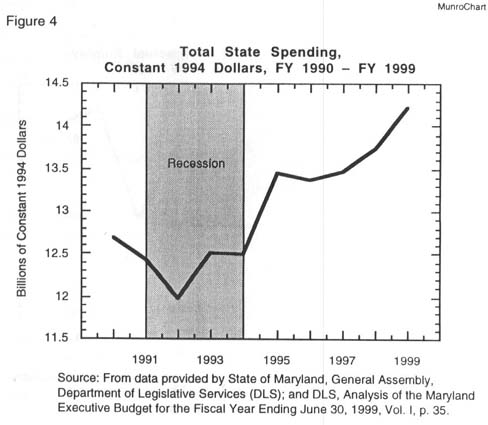

Likewise, real expenditure growth was only temporarily abated during the recession. Expressed in constant 1994 dollars, total state expenditure of all funds was $12.7 billion in FY 1990. In FY 1995, shortly after recovery had set in, disbursement had reached $13.4 billion. Total spending for FY 1999 is projected at $14.2 billion, as shown in figure 4.13 (The nominal-dollar expenditures for FY 1990, FY 1995 and FY 1999 are, respectively, $11.2 billion, $13.8 billion and $16.5 billion.)

{kind=link}

The fact is, the state did not seriously make long-term adjustments in response to the recession. The government organizational chart looked much the same in 1994 as it had done four years earlier, despite the efforts of the Governor’s Commission on Efficiency and Economy in Government (discussed below). The organization of the executive branch in FY 1997 was virtually identical to its organization in FY 1990 – except bigger. In other words, recession forced the old gas-guzzler temporarily to drive at 55 m.p.h. to conserve fuel. That is all. Once the revenue embargo was lifted, the pedal could be – and was – pushed back down to the metal. We hold that it is time to take the old jalopy off to the scrap yard, to be replaced by an altogether more aerodynamic and fuel-efficient model.

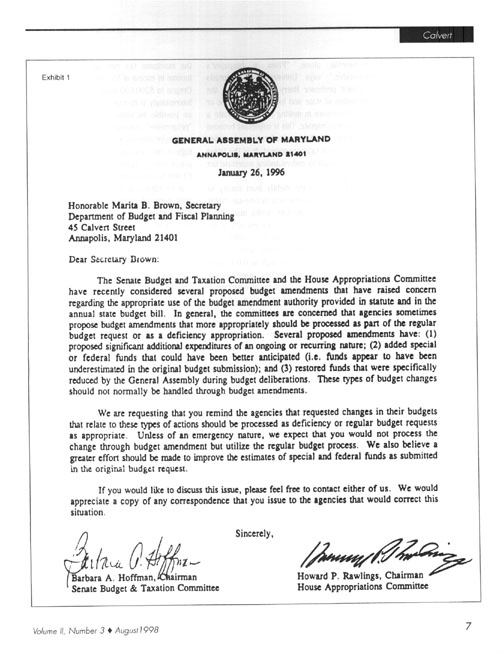

To this day, government scope and budgetary propriety are not taken sufficiently seriously in this state. In January 1996, Senator Barbara A. Hoffman (D-Baltimore County), chairwoman of the Senate Budget and Taxation Committee, and Delegate Howard P. Rawlings (D-Baltimore City), chairman of the House Appropriations Committee, chided the executive branch for introducing post facto budget amendments months after approval of the annual budget, thereby making budget scrutiny difficult. These amendments had, said Hoffman and Rawlings, “(1) proposed significant additional expenditures of an ongoing and recurring nature; (2) added special or federal funds that could have been better anticipated …; and (3) restored funds that were specifically reduced by the General Assembly during budget deliberations. These types of budget changes should not normally be handled through budget amendments.”14 All told, the picture painted was of an executive branch anxious to avoid in-depth legislative scrutiny of its proposed spending. (The letter is reproduced in exhibit 1.)

{kind=link}

Fiscal debate in Maryland revolves almost exclusively around questions of revenue. The expenditure component of the fiscal equation has gone largely unnoticed – by the media and by Annapolis. This essay remedies this defect. It presents a blueprint for reduced state spending in Maryland. If Maryland’s disease is ever-expanding government, characterized by the twin symptoms of high taxation and excessive borrowing, then we propose a cure – a cure that would allow this state to buy back all outstanding general-obligation debt over two gubernatorial terms while still allowing funds for immediate and substantial tax relief, starting in FY 2000 with a 7.48 percent cut from projected income-tax revenue estimates for that year and continuing to FY 2007 with a 20.21 percent cut. (In other words, implementing our reforms would reduce the state’s reliance on projected income-tax revenue by 20.21 percent in FY 2007.) Tax reductions from current revenue estimates would continue after that, increasing annually from $1.03 billion in FY 2007.

II. The Symptoms: Taxes

Prior to the recent, modest amendments to the tax code, enacted during the 1997 legislative session at the instigation of Governor Parris N. Glendening (D), the situation for Maryland taxpayers was as follows: Maryland’s lowest income-tax rate was 2.0 percent; its highest, 5.0 percent – or 2.4 percent and 8.0 percent if local income taxes are included, depending on the county.15 Maryland is one of only a handful of states that permit local governments to levy income taxes (known locally as “piggyback taxes”), so its combined rates of state and local income taxation are often compared to other regions’ income taxation levied by state governments alone. “From a taxpayer’s perspective,” says University of Colorado economics professor Barry Poulson, “it is the combination of state and local taxes that [he or she] will compare in making choices to locate a business or to migrate. This is important because comparisons are often made of state taxes, rather than state/local taxes combined. It is the latter which is relevant to understanding interstate tax competition.”16

Though rates vary slightly from county to county, Maryland’s lowest local income-tax rate is 20 percent of the state rate, which made for a lowest combined rate of 2.4 percent before the 1997 legislation. The state’s highest possible local rate is 60 percent of the state rate, which allowed a combined effective rate as high as 8.0 percent in some counties. (Most counties’ piggyback-tax rates are 50 percent or 60 percent of state rate or somewhere in between. Only two counties deviate: Talbot County, 40 percent in FY 1998; Worcester County, 20 percent, FY 1998.) The other states allowing local governments – sometimes municipalities rather than counties – to tax personal income are Arkansas, Delaware, Indiana, Iowa, Kentucky, Michigan, Missouri, New York, Ohio and Pennsylvania.17 For the purposes of this section, we take the term “Maryland income taxation” to include local income taxation.

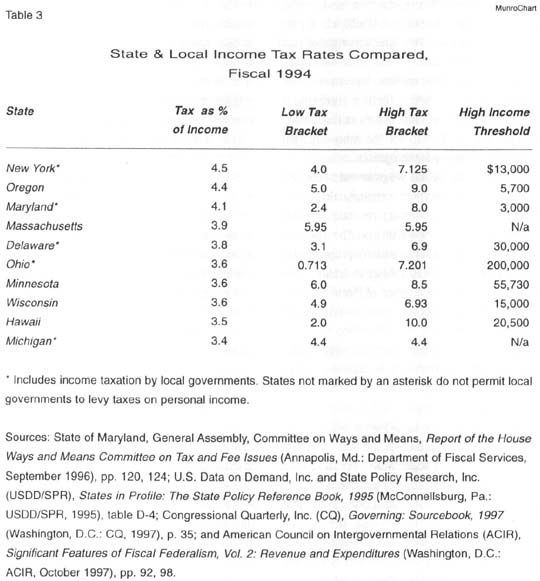

Table 3 presents the ten states with the highest individual income taxes in FY 1994. Even among these high-tax states, Maryland stands out. Before the recent alterations to the tax code, Maryland’s state/local income taxation proportional to income was $39.79 per $1,000 of income next to a U.S. mean of $23.92 per $1,000 (FY 1992).18 At four percent of personal income, Maryland had the third-highest personal income-tax rate in the nation.19 The impact of Maryland’s relatively high top income-tax rate is exacerbated by the fact that it begins imposing the maximum rate – as high as 8.0 percent before 1998, depending on the county – on all taxable income over $3,000. This compares very unfavorably with the other top income-taxing states, where the maximum tax rate applies to all taxable income in excess of $5,700 (lowest threshold) in Oregon to $200,000 (highest threshold) in Ohio. Interestingly, in its zeal to subject as much income as possible to state taxation, presumably for “progressive” purposes, Maryland has devised a very regressive income-taxation system, with its highest tax bracket capturing all but those in abject poverty. Relatively few people have below $3,000 in taxable income.

{kind=link}

In FY 1994, a total of $4.9 billion in state and local personal-income taxes was collected on $118.8 billion of personal income. Based on these data, Maryland would have to reduce income-tax revenue by over $800 million annually in order to remove itself from the top ten personal-income taxing states.20 The governor’s 1997 legislation originally proposed to reduce income taxation cumulatively by $990 million over five years.21

The governor’s initiative of 1997 initially proposed to reduce the state-only income taxation rate by 10 percent, whittling the top rate of 5.0 percent down to 4.5 percent by FY 2001. Local governments’ piggyback rates were to have been excluded from the legislation, allowing them to continue levying income taxes at the old rate.22 Assuming that no county cut its piggyback taxes, the combined maximum rate would thus have fallen from 8.0 percent to 7.5 percent. This was in considerable contrast to the plan proposed by the administration’s own Department of Business and Economic Development, which proposed that a 25 percent income-tax cut be phased in by FY 2005.23

However, even the governor’s diluted tax plan failed to pass muster in the General Assembly. After considerable wrangling in the legislature, the plan to reduce the top rate to 4.5 percent was abandoned, with the new target being set for an altogether more modest reduction to 4.75 percent. Forces opposed to the tax reduction instead raised the personal exemption from $1,200 to $2,400 rather than enact the originally planned top-rate reduction, thereby somewhat lessening the regressiveness of the Maryland tax code. Taking these actions into account, the new combined state and local top rate will be 7.75 percent. (The decoupling of piggyback rates from state rates went into effect as planned.) During the 1998 legislative session, the tax-cutting schedule was accelerated to three years.24

However, there is some reason for doubt as to whether or not the full package will ever be ushered in. Last year, the top rate was reduced to 4.95 percent. The new schedule for rate reductions reduces this to 4.875 percent for tax year 1998 and to 4.85 percent for tax year 1999.25 In the meantime, the size of the exemption is gradually being raised. The actions of 1998 have accelerated the process somewhat, but have not altered the fundamental fact that the bulk of the cutting comes in the “out years” (i.e., later in the process). The governor has never identified what program cuts he intends to implement to make the full tax reduction possible.

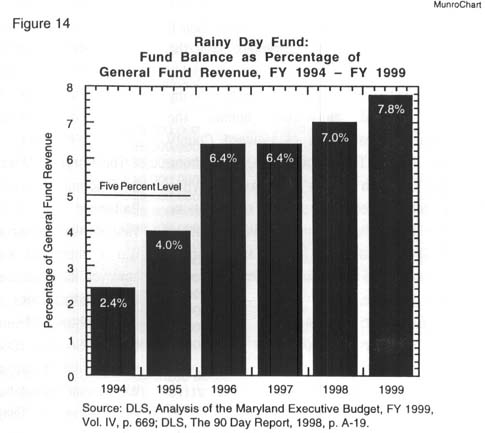

The entire accelerated tax cut so far has been financed by drawing $170.7 million in FY 199926 from the Revenue Stabilization Account (the so-called “rainy day fund”) to cover potential revenue loss and by taking advantage of 1998’s higher-than-expected state revenues. There exists a “Citizen Tax Reduction and Fiscal Reserve Account,” the purpose of which is in part to fund such tax cuts. This fund was created just after the last election – and then seemingly forgotten. Only $10 million has ever been appropriated to the fund,27 thereby rendering it useless as a source of funding for tax reductions. This explains the need to use the rainy-day fund as a source of money for the present round of tax reductions, for no actual program cuts have yet been made. The governor’s original calculations supposed four-year offsetting revenue of $286 million from a new cigarette tax. The tax was never enacted. The administration’s proposal also vaguely referred to $276 million in “other” cuts not identified. The Department of Fiscal Services calculated that the “other” cuts would actually need to be on the order of $698 million.28

Many skeptics consider Annapolis’ acceleration of the tax-cutting schedule to be typical election-year politics. If Annapolis refuses to commit to the program cuts necessary to fund a tax reduction, how serious can the establishment be? Skeptics further note that, prior to the last election, Annapolis passed legislation creating the Efficiency 2000 Commission, a task force charged with identifying areas for enhanced government efficiency and areas for budget cuts. The creation of the commission – discussed in detail below – was necessary for public-relations purposes, given the legislature’s flat refusal to act upon the recommendations of the similarly charged Butta Commission, which had been created in the wake of the disastrous 1991-1993 recession. Despite the fanfare surrounding the efficiency commission, legislators upon re-election quietly abolished it. Since that time, Annapolis has avoided any effort to make cuts in the size of state government.

Given the governor’s reluctance to identify the program cuts necessary to finance his tax reduction, and given the fact any such cuts are postponed until after the November 1998 election, some Marylanders assume that the rest of the tax cut will be shunted to one side after the election. In 1999, the assembly intends to re-examine the issue “to determine how quickly to cut the remaining 4 percent….”29 The governor’s lukewarm approach to tax reform is widely held to have been a primary cause of the recent resignation of his secretary of business and economic development, James T. Brady.30

If the skeptics are correct in their assumptions about the governor’s intentions – or lack thereof – in regard to seeing through the tax cuts promised, then the situation outlined in table 3 will remain substantially unchanged. The high income-tax rate will, in the words of the Brady report, continue to serve as a “red flag” to businesses considering moving to Maryland. The state’s negative business image, described in detail two years ago by the Department of Business and Economic Development,31 will be retained.

IIl. The Symptoms: Debt

Entering FY 1999, Maryland owes $3.3 billion in general-obligation debt, as noted previously. Forecasts show that this amount will increase to $4.5 billion by the end of FY 2007.32 This is due to Annapolis’ habitual use of 15-year debt financing on bond issues to fund capital programs. Only the state’s operating budget is subject to the constitutional balanced-budget requirement. This is not the case with the capital budget. The capital budget – funding used for big-ticket construction projects and the like – is partly financed by means of bond sales. Borrowing funds for capital projects frees up operating-budget funds for program expansion.

The current $3.3 billion debt refers only to state general-obligation debt – tax-supported, 15-year debt used in part to build, improve and equip state and locally owned capital facilities and in part to provide grants and loans to non-public entities. There is further debt, however – debt associated with highway construction and maintenance. The gas taxes, vehicular titling and registration fees that finance this debt are not discussed here.

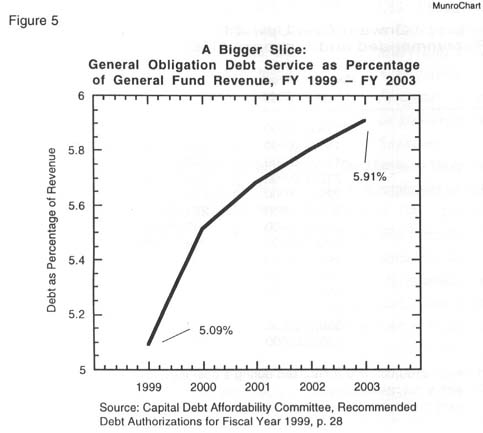

Revised figures indicate that in FY 1998 it cost Maryland taxpayers $417.8 million to make the principal and interest payments on the existing $3.3 billion debt,33 which is about $165 for every taxpayer in the state.34 (Earlier estimates had predicted $423.5 million.)35 During FY 1999, the debt will increase to $3.5 billion, necessitating $418.5 million in principal and interest payments,36 optimistically assuming a continuation of current low interest rates. Maryland has committed itself to staying in debt well into the next century. As figure 5 shows, general-obligation cumulative debt as a percentage of state anticipated revenue will increase from 5.09 percent in FY 1999 to 5.91 percent in FY 2003.37

{kind=link}

Naturally, borrowing is sometimes required. However, given the costs of borrowing, we recommend increased reliance on another way to fund projects – using existing revenue, at least to a greater degree than is currently the case. PAYGO expenditures for state capital projects in fiscal 1999 will total $1.16 billion.38 This means spending on a pay-as-you-go basis out of current revenue, with no 15-year debt. Perhaps if voters were made more aware of the long-term costs of borrowing they might be more inclined to demand accountability and restraint. What does borrowing cost? To illustrate, on July 30, 1997, the state sold $250 million in bonds at an interest rate of 4.6396 percent.39 Every $1,000,000 borrowed will cost $1,446,852 to repay in principal and interest over the 15-year life of the loan.40 By the time that June 1997 bond issue of $250 million is fully repaid 15 years from now, it will have cost Maryland taxpayers $361.7 million. That is, $250 million in principal payments and $111.7 million in interest payments. (To put this in some perspective, assuming average salary and benefits of about $40,000 per year, $111.7 million would fund 195 new public school teachers for 15 years.)

Given ever-escalating debt costs, we recommend – at minimum – limiting annual new debt to annual debt redemption. In other words, no new dollar of debt should be incurred without paying off a full dollar of old debt. At its inception back in 1978, the Capital Debt Affordability Committee (CDAC) – an advisory group made up of four government officials and one-private sector member41 – advanced this idea. The committee dropped the idea nine years later. This was principally because there were stadiums to be built, because rating agencies seemed content to give Maryland a triple-A bond rating despite high borrowing requirements, and because adherence to the policy of paying off an old dollar before borrowing a new one tied yearly authorizations to events of 15 years previously. This was held to produce highly variable bond authorizations from year to year, which was said to be inconsistent with either good management or a stable capital program.42 The result has been an endless routine of borrowing upon borrowing ever since. This is ironic, to say the very least. It was this sort of behavior in the 1970s, seen by many as reckless, that had led to the creation of the CDAC in the first place.43

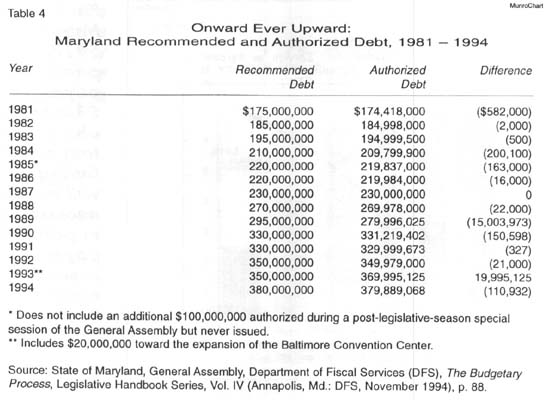

Shortly after the CDAC’s abandonment of the old policy, evidence of Annapolis’ appetite for borrowing was apparent during the recession of the early 1990s. Given Maryland’s constitutional requirement for a balanced operating budget, spending had to be curtailed. Cumulative baseline spending reductions over the period 1991 through 1993 totaled $2.1 billion.44 Every imaginable idea for reducing state spending was suggested – and some of these ideas were even enacted. But this frugality logic did not extend to borrowing. As table 4 illustrates, despite the fiscal crunch, the assembly continued to rack up debt.45 The CDAC’s debt recommendations have increased by about six percent a year, as has the legislatively approved debt.

{kind=link}

In addition to adopting a policy of increased reliance upon PAYGO for capital projects, debt-financing should be tied to the state property tax. Maryland’s constitution requires the imposition of a tax to finance annual debt-service costs.46 The tax imposed for this purpose is the state property tax, set at 21¢ per $100 of assessed valuation. All the proceeds from the state property tax are credited to the Annuity Bond Fund for general-obligation debt retirement purposes. But Maryland’s annual debt obligations far exceed available state property-tax revenue. Of FY 1998’s debt-service costs of $417.8 million, only $240.8 million (57.6 percent) was derived from the state property tax. The other $177.1 million (42.4 percent) was primarily taken from the state’s all-purpose general fund.47

As such, this debt-service cost is arguably hidden from taxpayers. Maryland’s budget documents are obtuse to the uninformed reader and are for the most part not broken down to show line items. As a practical matter, paying off old debt with general-fund moneys or with new debt greatly reduces the need to explain the original obligation. The legislative analysis of the FY 1998 budget notes dryly a 4.1 percent increase in debt-service needs and penalty/rebate payments relative to fiscal 1997. But it makes no attempt to explain the rationale behind the expenditure that necessitated the borrowing to start with.48

In spite of the convenience of camouflaging debt servicing within the general fund, its divorce from state property-tax revenues would appear to be contrary to the law, as previously noted by this organization.49 The enabling act which authorizes state debt is straightforward on this matter: “An annual State tax is imposed on all assessable property in the State in rate and amount sufficient to pay the principal and interest rate on the bonds, as and when due and until paid in full.”50 Indeed, the state attorney general has ruled that a bondholder would be entitled to seek legal action requiring the Board of Public Works – made up of the governor, the state treasurer and the comptroller of the Treasury – to collect sufficient property-tax revenues to meet the state’s debt-service obligations in full (rather than hiding the true extent of borrowing by drawing on the general fund and upon new bond issues to pay off part).51

In October 1996, the General Assembly’s financial staff agency, the Department of Fiscal Services (now the Department of Legislative Services), proposed this very notion in a special report to the legislature:52

Revenues generated from an increase in the State property-tax rate could be used to pay the additional cost of the general-obligation bond debt service. This would require an increase in the State property tax of $0.15 per $100 of assessed value, making the new rate $0.36 per $100 of assessed value. The increased property-tax revenues would then free up general-fund revenues that could be used to fund a tax reduction or to pay for other programs….

Since the property tax is deductible for federal and State income-tax purposes, taxpayers who itemize their deduction would realize an income-tax savings for a portion of the additional property tax paid.

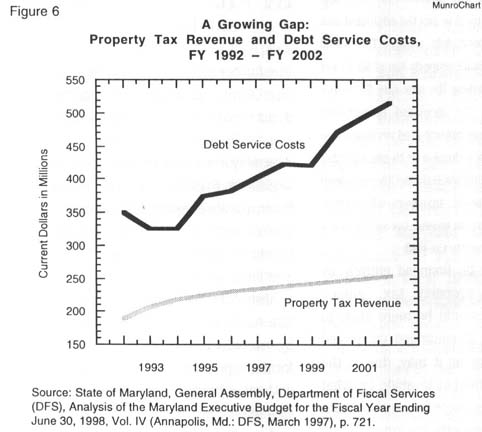

If borrowing had to be financed entirely by means of the state property tax, annual fluctuations in the levy would be more likely to cause residents to balk at continued unchecked bond floatations. Be that as it may, due to the state’s apparent disinclination to abide by what seem to be its own rules, there is a real concern that the gap between property-tax revenue and debt servicing will increase, meaning ever more borrowing hidden from taxpayers.Figure 6 tells the story plainly. In fiscal 1992, property-tax revenues covered 54.1 percent of debt payments. In fiscal 2002, such revenue is projected to amount to only 49.0 percent.53 To put this in some perspective, in fiscal 1966 property-tax revenue accounted for no less than 89 percent of debt service.54 Based upon September 1996 projections, figure 6 shows escalating annual debt payments reaching $515.6 million by 2002,55 though subsequent research indicates that the 2002 figure will in fact be higher ($519.1 million).56

{kind=link}

Despite this, ever-increasing borrowing into the 21st century is anticipated for the foreseeable future. Figure 1 in chapter 1 shows ever-increasing proposed borrowing authorizations through 2007. For 2007, borrowing authority of $565 million is suggested, a number 31.4 percent higher than this year’s borrowing.57 A symptom of Maryland’s penchant for a large public sector, Maryland’s debt policy is characterized by growth, not restraint. Currently, nowhere on the horizon is evidence of fiscal restraint to be seen.

IV. The Symptoms: Mandates and Local Aid

One further symptom of Maryland’s ailment is the legislature’s proclivity for mandating certain items of spending. Just how much does Maryland mandate? The question was posed to the General Assembly’s accounting arm, the Department of Legislative Services (DLS), by Delegate D. Bruce Poole (D-Washington) last summer. Apparently, Poole’s request represented the first time any legislator had thought to ask. “The answer was startling,” wrote Poole in an article on the subject published by the Calvert Institute.58 The fact is that nearly half of all state spending is mandated by law, which is to say that annual expenditures for these programs are automatically authorized, without program proponents’ having to go through the inconvenience of legislative hearings and the like. In terms of the general fund, more than one of every two dollars is mandated.

Mandated spending for the just ended FY 1998 within each of the state’s three sources of revenue – general, special and federal – was as follows:

- 56.7 percent of all general-fund spending, $4.42 billion out of $7.78 billion.

- 26.2 percent of all special-fund spending, $1.10 billion out of $4.20 billion.

- 35.8 percent of all federal-fund spending, $1.23 billion out of $3.45 billion.

In sum, 43.7 percent of total state spending in FY 1998 in all categories was mandated, no less than $6.75 billion out of $15.44 billion.59

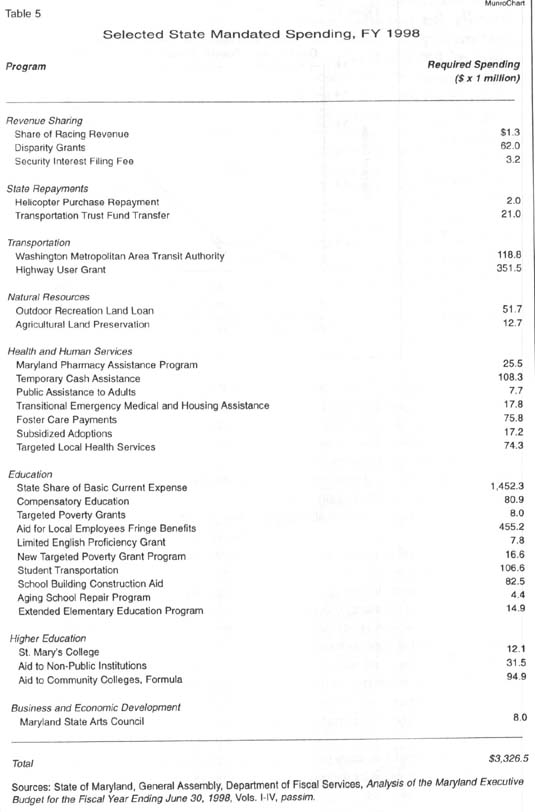

A selection of Annapolis’ annual, mandated payments is shown in table 5 , in this case for FY 1998. Regardless of the merit of some of these programs, the fact is that, by enshrining their funding in perpetual law, accountability is lost. In government, as elsewhere, the maxim “out of sight, out of mind” applies in force. Mandated program expenditure is, in effect, out of sight – and so out of mind. Because spending is automatically authorized every year unless some legislator proposes amending legislation to terminate a program, many of these policies are rarely revisited by the assembly once passed. As Delegate Poole puts it, such expenditure is “often not debated or otherwise subject to the ordinary trappings of the discussion process.”60 As can readily be imagined, this sort of approach to state budgeting does not lend itself to frugality. It is one of the reasons expenditure is so chronically high in Maryland.

{kind=link}

Observant readers will note from table 5 that a large proportion of mandated expenditure is on programs making payments to local governments. Examples include aid to community colleges and a vast array of K-12 education grants. So it is not surprising to find out that state assistance to local governments has increased relentlessly over the past few years. This is despite the fact that county governments in Maryland are relatively self-sufficient compared to their counterparts in many other states.

As previously described, few states permit local income taxation, an advantage for the purposes of local self-sufficiency. Collectively, Maryland’s local governments are above average in terms of self-sufficiency from all taxation sources, drawing local taxation equal to 4.8 percent of personal income, compared to 4.7 percent for local governments nationwide. In terms of income taxes, Maryland’s local governments receive income taxes representing 1.4 percent of personal income – far and away the highest rate of local income-tax return in the country. Among states permitting local income taxation, the average return as a percentage of personal income is 0.2 percent. The states whose localities that come closest to matching Maryland’s counties in income taxation are New York and Pennsylvania, for which local income taxation amounts to 0.8 percent of personal income.61

Maryland’s local governments can hardly be said to be experiencing fiscal pain currently. At the end of FY 1997 (that is, in June 1997), local governments were enjoying their largest aggregate general-fund surplus in a decade.62 This is evidenced by the fact that no county has increased local taxation recently. In fact, in FY 1998, four counties – Allegany, Carroll, St. Mary’s and Worcester – reduced their piggyback income taxes. At the same time, five counties – Caroline, Dorchester, Prince George’s, Queen Anne’s and, again, St. Mary’s – reduced their property-tax rates.63

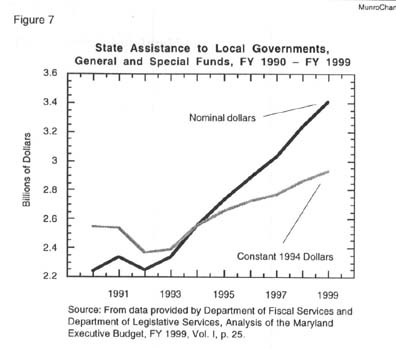

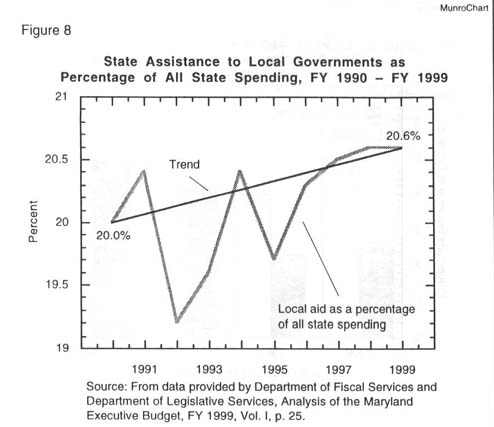

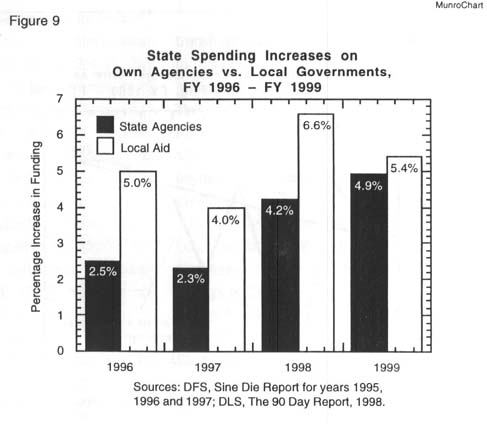

Regardless of the counties’ current fiscal bounty, as figure 7 shows, state payments to local governments have risen from about $2.2 billion in FY 1990 to some $3.4 billion in FY 1999 for an increase of 54.6 percent (or about $2.55 billion to about $2.95 billion in 1994 dollars for a real increase of 15.7 percent).64 As a percentage of all state spending, figure 8 shows that local assistance has fluctuated considerably over the past few years. This said, the trend has been upward, increasing from 20.0 percent of state spending in FY 1991 to 20.6 percent in FY 1999.65 Figure 9 shows that every year from FY 1996 through FY 1999, the annual increase in local aid has surpassed – sometimes substantially surpassed – the annual increase in spending on state agencies.66 A serious question should be posed in Annapolis: If local government coffers are now so flush with funds that local taxes can be cut, why, other than for electioneering purposes, is state expenditure on local aid increasing so rapidly?

{kind=link}

{kind=link}

{kind=link}

As long as much of this aid is mandated by state law, and as long as local governments have no incentive to economize in the expenditure of such aid, the size of state government will not shrink without drastic action. Mandating severely restricts legislators’ budget flexibility, while escalating local aid results in a decoupling of the pleasure of spending (counties) from the pain of taxation (state), a recipe for runaway spending – an issue to which we return below. It is as much for these reasons as any that past attempts to rein in spending, such as those discussed in the next chapter, have failed so miserably.

V. The Previous Cures

The recession is over. “The good news is that some of the economic indicators for Maryland are finally upbeat. The bad news is that a return to financial health is likely to short-circuit steps to reorganize and shrink state government in Annapolis.” This observation was made by editorial writer Barry Rascovar in a 1992 Baltimore Sun opinion piece.67 His words are just as apt today as they were then. When times are good, touchy discussions about downsizing government seem somehow less important. Most assuredly, this state has not had – at least has not seriously had – such a discussion in years. In fact, as recently as May 1998, the administration’s recently resigned secretary of business and economic development said, “One of the mistakes we are very capable of making now is to assume that, because the economy is going well [currently], we’ve solved all of our problems.”68

The most important reorganization of state government since World War II occurred in 1969. That year, Maryland’s government was transformed from a fragmented system of 246 separate and autonomous units into a secretariat system, with agencies headed by a cabinet secretary answerable directly to the governor. The impetus for this change stemmed from the findings and recommendations of the Committee on Executive Reorganization, appointed by then-Governor Spiro T. Agnew (R) for the purpose of devising ways to streamline and modernize government functions. After Agnew’s departure to assume the United States vice-presidency, the committee’s recommendations were implemented under the administration of Governor Marvin Mandel (D), who succeeded Agnew.

The secretariat system, or cabinet form of government, began with the creation of four principal departments in 1969: Health and Mental Hygiene, Natural Resources, Budget and Fiscal Planning, and State Planning. In 1970, the number of departments increased by seven: Employment and Social Services, General Services, Personnel, Public Safety and Correctional Services, Licensing and Regulation, Transportation, and Economic and Community Development. The size and scope of state government has increased considerably since then. When Governor William Donald Schaefer (D) left office in January 1995, there were 16 departments and 43 agencies.69 The executive branch is currently made up of 16 main departments and no fewer than 79 independent agencies and commissions,70 which is to say that the number of these latter agencies has almost doubled over the past four years. (In addition, there are now 37 executive committees, task forces and advisory boards.)

There have been sporadic attempts since 1969 to implement further government reform. On September 12, 1991, executive order 01.011991.29 was issued by Governor Schaefer. This created the Governor’s Commission on Efficiency and Economy in Government, generally known as the “Butta Commission,” after its chairman, J. Henry Butta. Amid much fanfare, the Butta Commission was charged with:

- Conducting a review of state programs and operations with a view toward making recommendations for program elimination and general government downsizing;

- Conducting a review of management practices in state agencies with a view toward making recommendations to improve efficiency; and

- Examining and analyzing staffing patterns within state agencies with a view toward making recommendations to eliminate duplication and inefficiency.

Despite hard work and solid recommendations, the Butta Commission accomplished precisely nothing. Its 115 cost-saving recommendations were consolidated into 40 bills by the Schaefer administration, which between them would have saved taxpayers $40 million. But the General Assembly almost entirely ignored the Schaefer/Butta package, passing only a handful of the bills. “There was no reorganization of state government,” said Senator Laurance Levitan (D-Montgomery).71 “The legislature said they weren’t interested,” mourned Butta himself.72

Simultaneously, the then-speaker of the House of Delegates, R. Clayton Mitchell, Jr. (D-Kent), released a report describing a proposed reorganization of government which purportedly would have resulted in FY 1993 savings of $46.7 million.73 The effort went nowhere.

The assembly’s disinclination to heed the Butta or Mitchell recommendations led the following year, presumably during a brief period of shame, to the statutory creation of the Efficiency 2000 Commission, known as E2C. At the time, the Baltimore Sun correctly noted, “Ways have to be found to cut government spending….” It continued, again correctly, “But overcoming the opposition of powerful special interests and status-quo lawmakers will be a formidable challenge.”74

The following year, cuts were made – but only to E2C itself. Annapolis must have found itself uncomfortable with some of the issues discussed by E2C staff: that Maryland at the time was the only triple-A bond-rated state with absolutely no methodology whatsoever for public-sector performance measuring,75 for example, or that the state owned and operated 18 print shops when one would have sufficed.76 So during the 1995 legislative session, the commission’s staff was reduced from six to two and its funding was only extended for a further six months. No commission members were ever appointed. Then on May 5, 1995, the new governor, Parris Glendening, abolished the commission altogether (despite its not being slated for termination until June 30, 2000).77 In short, E2C never even got off the ground. Glendening then created the Governor’s Council on Management and Productivity, a group shortly to be criticized for inactivity by at least one state legislator.78

During the same legislative session, 1995, legislation was enacted to consolidate all major environmental regulatory permitting activities into the Maryland Department of Environment.79 Additionally, two existing agencies were abolished – only to be replaced by two new agencies with virtually identical functions. The Department of Economic and Employment Development and the Department of Licensing and Regulation were revamped as Department of Business and Economic Development and the Department of Labor, Licensing, and Regulation.80

A year later, during the 1996 session, legislation was enacted to merge the Department of Personnel with the Department of Budget and Fiscal Planning, resulting in the new Department of Budget and Management.81 Simultaneously, certain boards and commissions were consolidated and/or abolished. The 12 separate Public Defender District Advisory Boards were merged into four Public Defender Regional Advisory Boards. Nine other commissions were abolished altogether.82

Most recently, during the 1998 legislative session, an independent agency called the Office on Aging, descended from the 1959 State Coordinating Commission on the Problems of the Aging, was promoted to cabinet status and renamed the Department of Aging.83

Today, the state government structure of 16 principal departments and 79 independent agencies is certainly an improvement on the pre-cabinet form of government, when the executive branch consisted of 246 independent and separate units. However, we contend that the time has come for further change. Clearly, as this chapter has demonstrated, budget savings are not a priority in Annapolis. After all, if nothing serious has happened in almost 30 years, how committed can the state government be to internal reform? We believe the time for real reform is long overdue. The succeeding chapters of this report demonstrate how this may be accomplished.

VI. The Calvert Cure

In this chapter, we present our cure for the Maryland disease. We propose that all the budget reductions described in chapter VII of this analysis be used to pay off the state’s general-obligation debt. Readers may recall that, during the Reagan presidency, there was disagreement between tax cutters and “budget hawks.” The former saw tax reductions as the first concern of government. The budget hawks, on the other hand, considered reducing the country’s budget deficit to be a priority; tax cuts would follow later. We suggest that, if budget cuts of sufficient magnitude are made, Maryland can have both – debt reduction and simultaneous tax cuts. As long as annual reductions from baseline levels of expenditure are larger than proposed new borrowing, headway can be made – eventually reducing the debt to nothing. In the process of reducing the debt, debt-service payments are naturally reduced. It is by means of reduced payments on servicing the debt that we fund our tax cuts.

Our plan will allow Annapolis to have paid off its general-obligation debt in its entirety by fiscal 2007. At the same time, the plan will result in first-year tax cuts of $321.5 million, a figure that rises to just under $1.03 billion annually by FY 2007. We are not aware of such a plan having been devised for any other state.

As discussed in chapter III of this report, the continuing use of debt financing to pay for capital projects is an inefficient use of resources. From 1990 through the present, the state has increased its “credit card balance” from about $2.0 billion to $3.3 billion (nominal dollars).84 This refers only to general-obligation bonds, not to the various other state loans. At present, total state debt on all bonds – that is, general-obligation, transportation, capital-lease and stadium-authority bonds – is $4.7 billion, a figure set to rise to $5.2 billion by FY 2003.85 Unless otherwise specified, all references to “debt” in this and the next chapter are to general-obligation debt.

While virtually all Marylanders recognize the financial advantages of paying off their credit cards, Annapolis’ most recent “credit card” projections foresee an increase of over $1 billion in Maryland’s cumulative general-obligation debt by fiscal 2007, two gubernatorial terms from now. Under the terms of this arrangement, annual debt-service costs – i.e., the state’s minimum credit card payments – are predicted to reach $633.5 million, compared to $418.5 million in FY 1999.86 In the process, the taxpayer cost of each dollar of additional debt spent by the state will increase from $1.82 in FY 1999 to $5.25. This chapter describes why Maryland should get out of general-obligation debt and how it can achieve this while simultaneously generating considerable funds for income-tax cuts.

Our focus is solely upon general-obligation debt, probably the least potentially profitable of all the state’s forms of debt. There is a slender possibility that stadium-authority bonds for the construction of stadiums and convention centers may make a decent return one day. Likewise, there is nothing to prevent the use of transportation bonds to fund items such as toll roads, upon which the state might make some money back. General-obligation debt is generally used to finance everything else, from public-school capital projects to historical preservation to “community projects” to the endless and ongoing cycle of providing funds to local governments “where a state interest or need has been demonstrated” (the latter, a loose criterion, to be sure).87

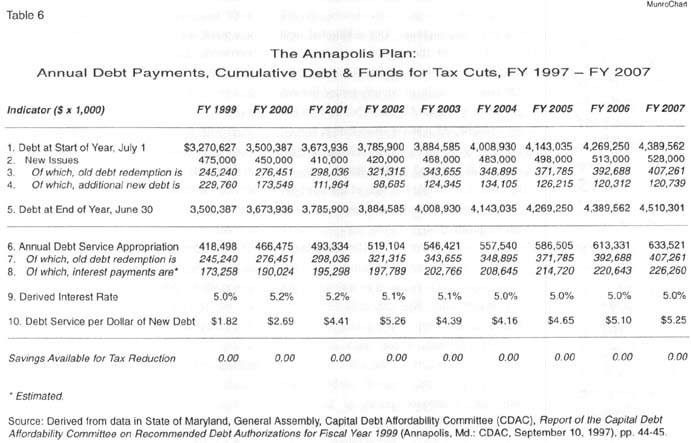

The Annapolis Plan

The projected growth in general-obligation debt, as reported by the Capital Debt Affordability Committee, is presented in the table 6. The table is not as complicated as it looks. Line 1 (“debt at start of year, July 1”) shows the cumulative general-obligation debt outstanding at the beginning of each fiscal year under discussion. These figures are taken directly from the CDAC’s analysis. Line 2 (“new issues”) shows the amount of new debt Annapolis plans to add to the cumulative debt every year. Again, this is taken from CDAC data. Annapolis’ annual new issues of debt go toward two things: paying off old debt and funding new capital projects. These are reflected in lines 3 and 4. Line 3 (“redemptions”) shows how much of the funding realized from new bond issues Annapolis anticipates using to pay off old debt every year. Annapolis in part uses new bonds to pay off old bonds, rather like using one credit card to pay off another. Line 4 (“additional new debt”) represents annual new issues overall minus annual redemptions. This additional new debt is put toward the annual capital budget (which is in total made up of PAYGO funds, debt on other types of bonds, previously issued but not yet redeemed general-obligation bonds and the new general-obligation issues described in line 4). Finally, line 5 is the general-obligation debt outstanding at the end of the fiscal year, 12 months later. It is simply the sum of the start-of-year cumulative debt plus the net new issues over the year in question.

{kind=link}

Moving on to the lower half of the table, line 6 (“annual debt-service appropriation”) shows the annual payment that is required as a result of the state’s past borrowing. Basically, debt service can be viewed as the required monthly minimum credit card payment. These data are taken directly from the report of the CDAC.88 Like a credit card payment, annual debt-service payments are composed partly of (a) some principal owed and (b) interest charges on all outstanding debt. Line 7 (“redemptions”) shows “a,” the principal redeemed. This figure is the same as line 3 in the top portion of the table. Knowing the debt-service requirements and knowing the annual redemptions, courtesy of the CDAC, allows us to subtract the second from the first to deduce “b,” the annual interest payments on Annapolis’ planned debt (line 8). From this, in turn, we can calculate the interest rate, which we find to vary between 4.9 percent and 5.1 percent (line 9). This is in accordance with historical data presented by the CDAC, which notes that for fiscal years 1995, 1996 and 1997, aggregate interest rates were 5.60 percent, 4.90 percent and 4.94 percent respectively.89

Finally, line 10 (“debt service per dollar of new debt”) is simply debt-service costs (line 6) divided by additional new debt (line 4). This gives us the ratio of new debt compared to debt service. For example, in FY 1999, additional new debt is $229.8 million and debt service is estimated at $418.5 million. The resulting ratio is 1-to-1.83, a crude measure of the cost of debt servicing to new debt, in this case $1.83 for every dollar borrowed. As the table shows, by FY 2007, Annapolis may be paying as much as $5.25 in debt-service costs for every new dollar borrowed and spent.

As with a credit card, the increasing balance owed (debt outstanding) has a proportional effect on the monthly credit card payment (annual debt-service payment). The more you owe, the larger your monthly minimum payment. In state government, the situation is no different. In FY 1999, Annapolis’ “yearly minimum” payment on its end-of-year debt of $3.5 billion will be $418.5 million. By FY 2007, the yearly minimum payment will be $633.5 million on a general-obligation debt load that will by that time have reached $4.5 billion. Because Annapolis has shown no inclination to control borrowing, the situation will escalate indefinitely after that. That is the Annapolis plan, such as it is.

The Calvert Cure

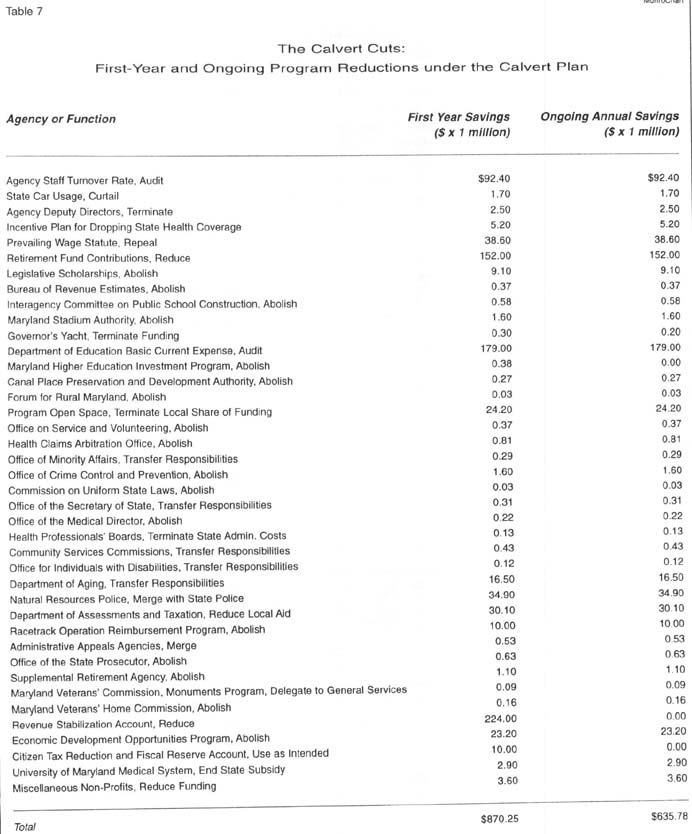

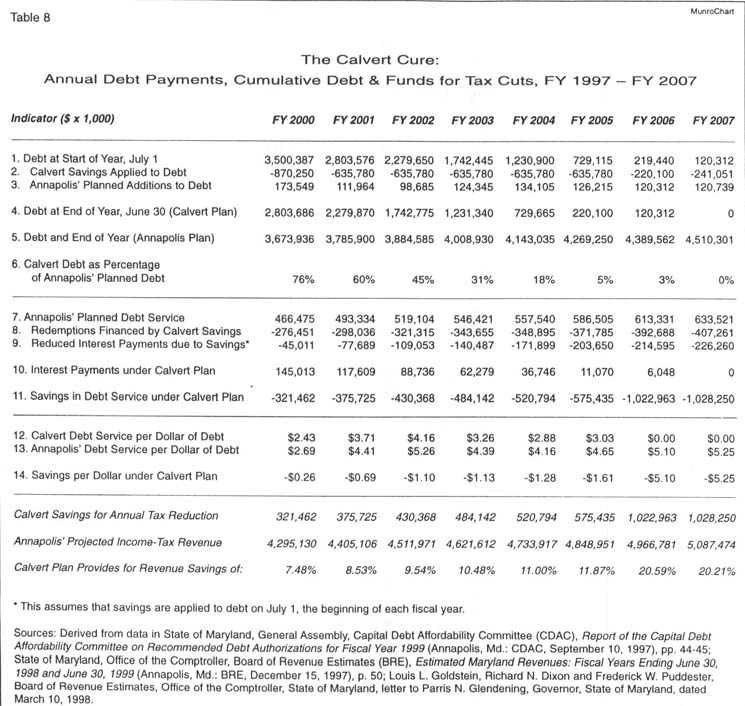

Instead, we propose something different, something daring. We propose to buy back every penny of state general-obligation debt while simultaneously providing millions of dollars’ worth of tax cuts. To accomplish this, we propose a first-year program reduction of $635.8 million plus a one-time transfer from the Revenue Stabilization Account of $224.0 million and the spending down of the $10.0 million in a little-known tax-reduction fund, for a combined debt-reduction package of $870.3 million. We then propose ongoing annual program expenditure thereafter set at $635.8 million below the current baseline, with the savings applied to debt reduction (total does not add up to detail because of rounding). A summary of our budget savings is shown in table 7 . The details are explained in chapter VII. Chapter VII provides a selection of cuts that could be made to finance the Calvert plan. It is not necessary that these be the actual cuts, though cuts of similar magnitude elsewhere would be necessary absent our suggested cuts. Our purpose is simply to raise ideas for serious discussion. (Alternatively, should Maryland realize significant revenue surpluses in the future, or should the state realize a significant windfall from any future legal settlement with tobacco companies, these funds could be utilized to achieve results similar to those described here.) Our plan as outlined herein would in its first year reduce state program expenditure by about five percent from baseline. Surprisingly, our plan retains many features of Annapolis’ planned expenditures, such as the general-obligation capital program, as shall be demonstrated below. The Calvert cure is described in table 8 .

{kind=link}

{kind=link}

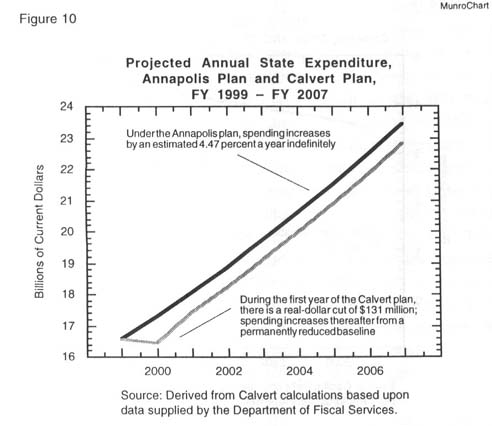

As shown in figure 10, under the Annapolis plan, state spending continues to grow every year, if precedent is anything to go by. From FY 1990 through FY 1999, state nominal-dollar expenditure increased by a weighted average of 4.47 percent a year. Projecting this growth into the future leads us to the assumption that by FY 2007 state expenditure will be $23.46 billion a year. Growth in government expenditure continues under the Calvert cure, too, but from a baseline permanently reduced by $635.9 million. Our first-year $870.3 million cut from baseline represents a real-dollar program cut estimated at $131 million, or a minuscule 0.79 percent, from the fiscal 1999 budget of $16.54 billion. Thereafter, we permit government growth at the same rate as under the Annapolis plan but from a permanently reduced baseline. Under the Calvert plan, state government spending would be $22.83 billion a year by FY 2007, a figure only 2.7 percent smaller than the equivalent figure under the Annapolis plan. Yet, our modest proposal is enough to get the state out of general-obligation debt completely and to provide the biggest personal income-tax reduction in Maryland history. The state should pay heed.

{kind=link}

Our plan enters fiscal 2000 at the same place one would enter it under the Annapolis plan, with cumulative debt of $3.5 billion. (See line 1, “debt at start of year, July 1.”) However, instead of putting $245.2 million of new bond issues into debt redemption, as under the Annapolis plan, our cure sinks $870.3 million of program cuts and interfund transfers into buying back old debt. This is described in line 2 (“Calvert savings applied to debt”). Generously, we permit the state to borrow $173.5 million in new general-obligation loans for the capital program (line 3, “Annapolis’ planned additions to debt”). This is the amount of new borrowing the government anticipated putting into the capital program under the Annapolis plan. Because the Calvert cure pays off debt with real money, instead of with more borrowed money, by the end of fiscal 2000 our plan sees the state with a cumulative debt of $2.8 billion (line 4, “debt at end of year, June 30”). This compares very favorably with the Annapolis plan’s expected cumulative debt of $3.7 billion by the same time (line 5). As line 6 shows, Calvert end-of-year debt is only 76 percent of the state’s planned debt.

It just gets better after that. The Calvert blueprint has the state entering FY 2001 with outstanding debt of $2.8 billion. We pay off $635.8 million of old debt, while allowing the state to keep its planned general-obligation borrowing for the capital program. This process is then repeated thereafter, paying off $635.8 million of outstanding debt a year and allowing capital-program borrowing to survive entirely unscathed throughout. Maintaining this regimen results in the cumulative debt’s being fully paid off in FY 2007.

Tax Cuts

The substantial tax cuts we propose are financed entirely through the reduced debt-service costs that automatically come about under our plan, demonstrated in the second portion of table 8. For example, line 7 shows that in FY 2000 the Annapolis plan calls for $466.5 million in debt-service payments. Our cuts of $870.3 million automatically pay off the $276.5 million the state was planning to pay off anyway, though our plan does it with real money not borrowed money. Thus we automatically cancel the principal component of that year’s minimum payment. Our estimate is that this reduces the interest component by a further $45.0 million. In sum, interest payments under the Calvert plan come to $145.0 million for FY 2000, compared with $190.0 million under the Annapolis plan (table 6, line 8). The sum of Calvert redemptions and reduced interest payments is $321.5 million (line 11, “savings in debt service under Calvert plan”). Under the Calvert cure, personal-income taxation would be reduced by this amount. We then subtract this from Annapolis’ projected revenue for that year, enabling us to describe our cuts as a percentage of anticipated revenue.90 In this case, our first-year revenue reduction would be 7.48 percent. (These figures present our tax cuts in the most conservative light possible because state projections taking into account the accelerated Glendening tax cut resulting from 1998 legislation are not yet available. This acceleration will depress revenue relative to the projections we have utilized here, meaning that our program cuts would in actuality represent a larger proportion of a smaller budget. In short, our cuts as a percentage of revenue would in fact be slightly higher than described here.)

As this process is repeated in subsequent years, the difference between cumulative debt under the Annapolis plan and under the Calvert plan gets larger. Every year, the debt under the Calvert plan is smaller relative to the Annapolis plan and smaller in actual dollar amount. This being the case, annual debt-service costs become progressively smaller under our plan. We continue to determine our tax cuts by the size of the difference between debt-service costs under the Annapolis plan versus debt-service costs under the Calvert plan. This difference becomes larger every year, allowing annual tax reductions to be increased annually.

Under this scenario, some time during FY 2006, the debt is paid off entirely apart from a small amount of new debt necessary to fund the capital program. Once this has happened, we no longer need to put $635.8 million a year into debt redemption – because there is no debt left. Only a relatively small amount (some $120 million annually) is needed to maintain Annapolis’ capital program, so at this point we continue applying debt-service reductions to tax cuts but we also add in our now redundant debt-redemption payments. This results in a tax cut of $1.02 billion in FY 2006 and a cut of $1.03 billion by FY 2007. By FY 2007, the Calvert plan will have produced a tax cut equaling 20.21 percent of Annapolis’ projected revenue for that year. Our cuts as a percentage of revenue would escalate from this point on, though definite projections are difficult.

An alternative means of providing tax cuts to Marylanders would simply be to use our program savings for direct tax reductions, as opposed to leveraging tax cuts by means of debt purchasing. Despite initial appeal based on simplicity, this would over the long term produce tax reductions of smaller magnitude for residents. First-year tax cuts would be 20.3 percent of projected FY 2000 revenue. But by FY 2007, the cut would only be on the order of 12.5 percent of projected revenue ($635.9 million divided by $5.09 billion). From this point on, $635.8 million as a percentage of projected revenue would become smaller and smaller, resulting in tax reductions of an ever shrinking percentage. By contrast, under the Calvert plan, program cuts combined with savings due to the elimination of interest payments would result in reductions from projected revenue of well over a billion dollars a year.

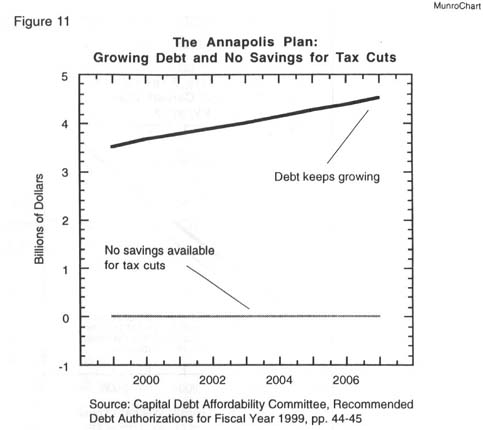

This is the Calvert cure. The radical difference between the Calvert plan and the Annapolis plan for debt upon more debt is vividly demonstrated in figures 11 and 12. As figure 11 shows, Annapolis’ plan for Marylanders is ever-higher debt and little else. Our proposal is for a reasonably painless way to eliminate the general-obligation debt and to produce a tax cut of a level unprecedented in Maryland history (figure 12). The Calvert cure promises relatively less government spending and a greater retention of hard-earned dollars for taxpayers. The Annapolis plan promises the exact reverse.

{kind=link}

{kind=link}

VII. The Prescription

In this final chapter, we present our specific recommendations for program cuts and other savings. As noted in chapter VI, these total some $870.3 million for the first year and $635.8 million a year thereafter. Implementing these cuts and savings would enable the state to buy back all outstanding general-obligation debt, thus freeing up hundreds of millions of dollars annually for tax cuts, funds that otherwise would have been necessary for debt-service payments. While our cuts are of significant magnitude, they are in fact very conservative. To the degree possible, we consider only savings to the general fund. For example, Maryland has no fewer than three health-care regulatory commissions located within the Department of Health and Mental Hygiene.91 While there is a case to be made for abolishing them, we do not consider them herein. This is because they are funded by means of fees levied upon the medical sector, with costs subsequently passed down to consumers. However, as terminating these commissions would not save general-fund moneys, this essay does not examine them. In some instances, however, funding sources are interwoven and state budget documents are not detailed enough to allow us to segregate them.

We are fully cognizant that the political opposition to our recommendations would be vast if a governor or legislator were to follow through on implementing them. We fully understand that every inefficiency has a constituency (often a very vocal and politically powerful constituency), while average taxpaying Marylanders are, for the most part, quiescent and uninformed. For Annapolis, the easy way out, then, is to maintain the status quo – however damaging.

We present here a variety of recommendations. Some are relatively inconsequential; some, of great consequence. Some are complex; some simple. While all of our recommendations will be opposed by someone, somewhere, some of our suggestions will be more controversial than others. For example, we recommend the termination of a number of the state’s many economic-development programs. Each will have its staunch defenders, no doubt, but nonetheless many reasonable people will, as a gut instinct, recognize that duplication in government is generally an undesirable trait.

On the other hand, other of our suggestions will engender colossal opposition, despite the fact that the particular situation in question is scarcely defensible as a matter of logic. The local education agencies’ apparently routine “over billing” of the state for mandated intergovernmental fund transfers falls into this category. We conservatively estimate that this over billing is to the tune of $179 million annually. Woe betide the politician who tried to remedy the situation, however. The public education establishment’s full political might would be mobilized in an instant. Thousands of dollars in campaign funds would be channeled to whomever the next opponent might be of the naive incumbent who dared to suggest that the mandated distribution of education funds should be based upon correct accounting by local public school systems.

Aware of this, Annapolis has done nothing effective in the past. We use the word “aware” advisedly and in a dual sense. Annapolis is aware of the opposition that reform would create, to be sure; hence, its inactivity. But Annapolis is also fully aware of much of the content of this report. A large proportion of our analysis is taken from the forest of paperwork annually released by the Department of Legislative Services – and inevitably ignored completely. Our estimates of the savings that would result from auditing local education agencies’ requests for transfer funds; our estimates for the saving to be gained from abolishing “prevailing wage” rules for public construction projects; our estimates of the savings that would be wrought from consolidating administrative-appeals agencies – all these we have derived from state government sources, usually the DLS. So why has the state done nothing in the past? Inertia, perhaps; and fear, no doubt.

In many respects, this is the most disturbing aspect of our findings – not the fact that the state routinely squanders millions of dollars annually on questionable priorities, but that it does so in the full knowledge that it is doing so. To be wrong in ignorance is one thing; to be wrong and fully aware of it is entirely another.

A. Cross-Agency Issues

The issues listed immediately below cannot be categorized by branch or agency because they impact all areas of state government. Below, and indeed throughout this chapter, our headings indicate, first, the government branch of the program under discussion (cross-agency, legislative, executive, etc.); second, the type of administering agency (cabinet department, independent agency, etc.); third, the category of program (state aid to education, for example); fourth, the actual program (basic current expense formula payments, for instance); and finally, after the colon, our recommended action.

At the end of each section is a savings tally with two figures. The first figure represents the first-year savings that would result from our recommended actions; the second, the on-going annual savings. For the most part, these two figures are the same. Occasionally, however, the first year’s action would result in savings that could not be replicated. In these cases, the second figure, for on-going savings, is shown as being lower than the first-year tally. Our figures for out-year savings are obviously speculative – and very conservative. We assume that programs would have continued to be funded at the same level. This is in fact unlikely. Program expenditures usually increase, especially for mandated programs. Our out-year figures in all probability underestimate the savings that would be brought about by implementing our recommendations.

Within the text of each section, we often present very detailed savings figures; for the end-of-section tallies we have for convenience rounded to one decimal place for figures of over one million. For figures in the thousands, we round to the nearest thousand. Given that the nature of government is always to spend more, not less, we have rounded all figures up unless the detailed number in question was only minutely above a whole number (in which case, we have rounded down).

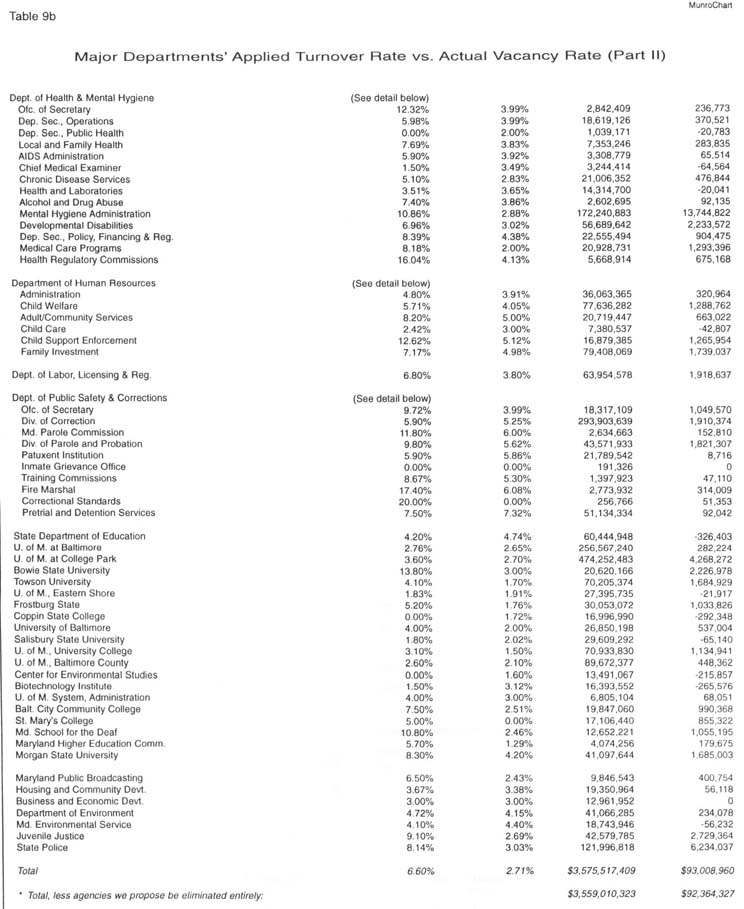

A1. Cross-Agency Issue o Agency Staff Turnover Rate: Audit

The fact is this: Just as Maryland’s local education agencies appear to over bill the state for students that do not exist (see section CC1), so all the evidence indicates that government agencies are over billing the state for employees that do not exist. As with the schools’ over billing, legislators are perfectly well aware of this; they just prefer to do nothing.

In a February 3, 1993 press release, then-House Minority leader Ellen R. Sauerbrey (R-Baltimore County) drew attention to the need for correct accounting of departmental vacancy rates.92 This was important, according to House Republicans, because agencies were typically under reporting their vacancy rates, leading to higher-than-justified budget appropriations for salaries. The GOP members claimed that annual savings of $35 million could be realized if budgetary reductions were made based on a true accounting of vacant positions.

House Republicans identified “a number of different possible implications of such large unspent payroll appropriations: (1) whether this payroll appropriation accounts for the sums of money government agencies tend to ‘find’ when they want to undertake new projects; (2) if unused payroll appropriations have been spent offering certain employees raises via reclassifications; (3) if the administration intends to actually fill these positions; and (4) why such a large surplus of funds has not been shown in calculations of FY 1993 reversions.”93 To this day, the problem has not been addressed. Furthermore, the magnitude of the problem is almost three times as bad.

On any given day, in any given agency, a certain number of authorized positions are empty. Perhaps one employee has retired and a replacement has not yet been hired. For any number of reasons, there are always a number of vacancies. When making their budget requests at the beginning of the year, agencies take into account that there will be some vacancies during the coming year. They reduce their salary and benefits requests accordingly. The amount they reduce the request by is based on what is known as the “applied turnover rate.”

Naturally, no departmental secretary can predict with absolute certainty how many vacancies will occur over the year and how long each will go unfilled. Nonetheless, historical precedent could be utilized to make a good guess. But it generally is not. Because vacancies do not draw salaries, it is not in the interests of department heads to maximize the anticipated number of vacancies. The smaller the applied turnover rate, the larger the salary appropriation. If end-of-year salary funds are unspent, they can be used for other purposes. In fact, there is frequently a wide discrepancy between the applied turnover rate and the end-of-year “actual vacancy rate.” The appropriated salary funds that are then not spent on these “ghost” employees represent a windfall to the agencies. Annapolis is well aware of this situation. In April 1998, for example, the chairmen of the Senate Budget and Taxation Committee and the House Appropriations Committee demanded that the assembly increase the turnover expectancy of the Revenue Administration Division (RAD), an arm of the Office of the Comptroller, from 2.71 percent (as requested by the RAD) to 2.86 percent (a more accurate reflection of its actual vacancy rate of 3.14 percent).94